Ending a marriage after twenty or thirty years is a profound financial disruption. For established households in Delaware, it means dismantling a carefully built foundation of joint investments, suburban home equity, and shared retirement timelines. The consequences of settlement mistakes can be long-lasting, and you have less time to recover from a financial miscalculation.

A Grey Divorce in Delaware County exposes your accumulated wealth to significant risk. Protecting your stability requires a strategic approach to marital property division, long-term tax exposure, and spousal support. Securing your independence means understanding exactly what is at stake before you begin negotiations.

Protecting your independence requires a rigorous evaluation of your post-divorce cash flow, asset liquidity, and healthcare costs. Attempting to untangle these high-stakes financial realities without a precise legal strategy can lead to difficult-to-correct mistakes that jeopardize your retirement.

While this page focuses on Delaware County, you can review our broader Grey Divorce in Ohio guide for a statewide overview of property division, support, and retirement-related divorce issues.

Understanding Grey Divorce in Delaware County

Ohio courts utilize equitable distribution to divide property fairly, though not necessarily equally. In a later-life divorce, ensuring fairness requires properly valuing complex assets rather than simply splitting accounts down the middle. Furthermore, spousal support remains highly discretionary and depends on a detailed review of your post-divorce cash flow.

Your case will be managed through the Delaware County domestic relations court system. Because local judges exercise broad discretion when interpreting Ohio statutes, presenting a clear, financially sound argument is critical. Understanding local court expectations directly influences how efficiently your assets are protected and your settlement is finalized.

Why Divorce After 50 Requires a Different Strategy

A divorce after 50 requires a different legal approach than a younger couple’s separation. For established families in this area, the strategy must shift from anticipating future career income to protecting the substantial wealth and home equity you already hold.

These practical realities dictate the focus of your settlement:

| Financial Reality | Why It Matters in a Senior Divorce |

| Shorter Recovery Horizon | There is far less time to rebuild savings or recover from avoidable losses after an unfavorable settlement. |

| Retirement Income Dependence | Post-divorce income will likely rely primarily on pensions, Social Security, and investment withdrawals rather than ongoing employment income. |

| Asset Preservation Priority | The legal strategy must focus on protecting accumulated wealth, since future earnings may not be sufficient to replace what is lost. |

| Liquidity Risk | Retaining high-value assets, such as a suburban home, does not necessarily provide the cash flow needed for everyday post-divorce living expenses. |

| Need for Long-Term Predictability | Financial instability is more damaging later in life, making stable support, manageable expenses, and reliable income especially important. |

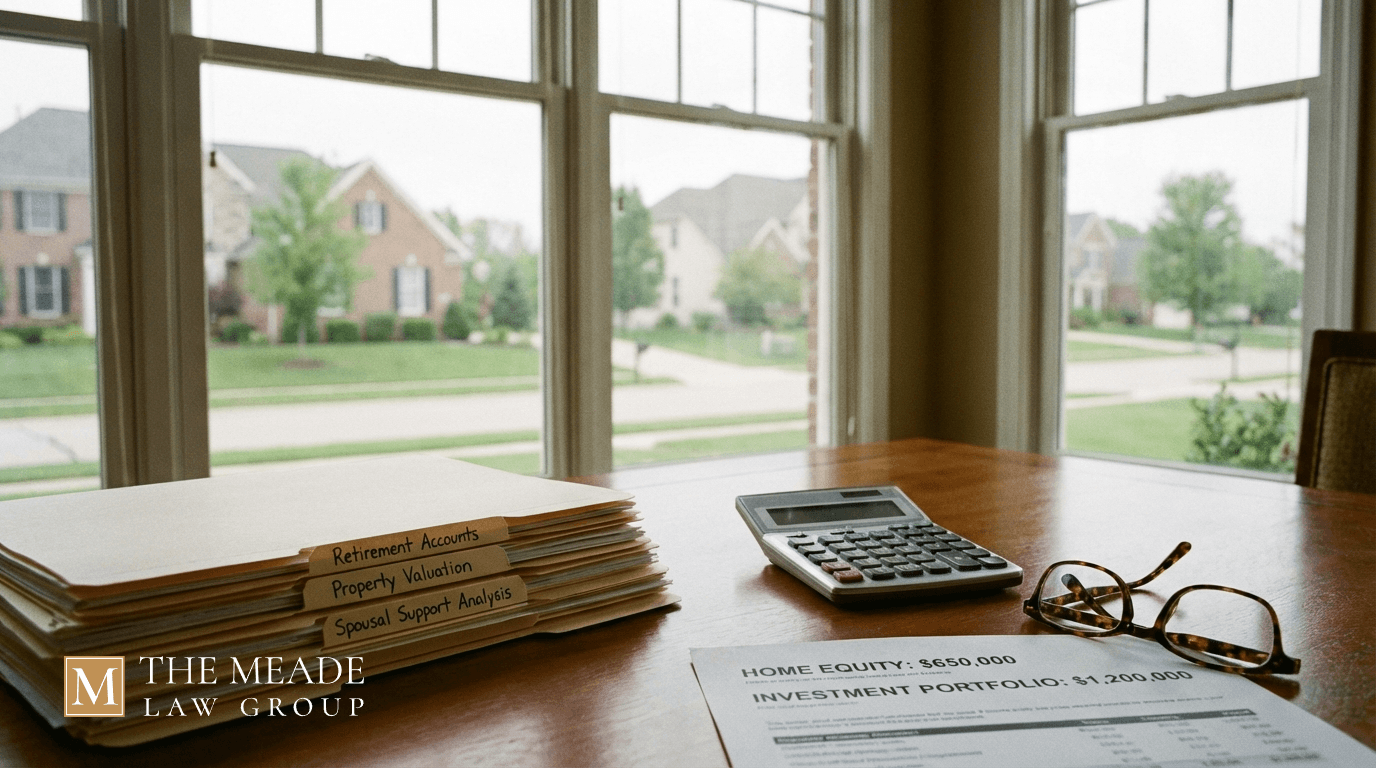

Dividing Marital Property in a Grey Divorce

In a divorce, established couples often have substantial home equity and investment assets built over many years. That makes property division more complex than simply assigning one asset to each spouse.

A sound division strategy must account for tax-adjusted value, liquidity, and long-term cash flow. An asset that looks valuable on paper can still create financial pressure if it does not provide the cash needed to support post-divorce living expenses.

A comprehensive division strategy must account for:

- Real Estate Holdings: The primary family residence and secondary properties often represent the most significant portion of accumulated wealth.

- Retirement Portfolios: 401(k)s, IRAs, and mutual funds require careful division to protect your long-term income stream.

- Pension Plans: Public or private defined-benefit pensions demand precise actuarial valuation to ensure a fair distribution.

- Business Interests: Closely held businesses or professional practices must be accurately appraised to protect your equity and operational stability.

- Executive Compensation: Deferred compensation packages and stock options carry complex tax rules that must be factored into their settlement value.

Retirement Assets and Pensions

Retirement assets are often the most significant part of the marital estate in a later-life divorce. For that reason, accurate valuation is essential to avoid an uneven result that undermines one spouse’s long-term financial stability.

These accounts often must be divided through a Qualified Domestic Relations Order (QDRO) so the transfer can occur without avoidable tax consequences or early withdrawal penalties. Mistakes in that process can reduce the value of the asset and affect retirement security well beyond the divorce itself.

Tax Consequences of Asset Division

Evaluating tax consequences is a central part of any property settlement. Two assets with the same face value can carry significantly different after-tax values, meaning a seemingly equal split could leave one spouse at a marked disadvantage.

You must actively plan for these tax exposures:

- Capital Gains Exposure: Selling highly appreciated real estate or long-held investments can trigger immediate and substantial tax liabilities.

- Retirement Transfer Risk: Executing retirement account transfers without a proper QDRO can result in severe IRS penalties and avoidable income tax bills.

- Deferred Compensation Treatment: Executive bonuses and stock options carry complex tax rules that must be factored into their settlement value.

- Investment Income Effects: The taxable income generated by retained investments will directly impact your post-divorce monthly budgeting and stability.

Financial Planning and Asset Valuation in a Grey Divorce

A sophisticated later-life divorce requires more than simply dividing property categories. It demands comprehensive financial forecasting to protect your Delaware County estate. The Meade Law Group recognizes that true fairness relies on identifying hidden risks, tracing separate property claims, and ensuring your settlement structure supports your long-term independence.

A strategic approach to high-asset divorce includes:

- Actuarial Pension Valuation: Calculating the true present and future worth of defined-benefit plans to prevent undervaluation.

- Executive Compensation Analysis: Securing your rightful share of complex corporate benefits, stock options, and delayed payouts.

- Business Practice Valuation: Utilizing forensic accounting to protect closely held businesses and professional practices from inaccurate appraisals.

- Marital vs. Separate Property Tracing: Clearly distinguishing pre-marital wealth and inheritances from assets acquired during the marriage.

- Tax Exposure Modeling: Forecasting the long-term tax liabilities associated with dividing heavily appreciated assets or liquidating retirement funds.

- Liquidity Planning: Balancing your need for accessible, immediate cash against the retention of long-term investments and real estate.

Spousal Support in Long-Term Marriages

In a long-term marriage, spousal support is often the deciding factor in whether a spouse can maintain their housing, medical coverage, and daily stability. Because an older spouse may face a reduced earning capacity after years out of the labor market, support obligations carry incredibly high stakes.

Under Ohio Revised Code 3105.18, courts evaluate several financial realities when determining support:

- Income and Earning Ability: Assessing each spouse’s realistic capacity to re-enter the workforce or increase their current earnings.

- Age and Health Conditions: Factoring in physical or mental health challenges that limit financial independence.

- Retirement Benefits: Evaluating the pensions, Social Security eligibility, and retirement income sources available to both parties.

- Standard of Living: Ensuring that the settlement avoids a drastic decline in financial stability for either individual.

- Duration of the Marriage: Recognizing that decades-long marriages often justify longer or indefinite support periods.

It is crucial to understand that retiring does not automatically terminate a spousal support order. Modifying or terminating these payments requires formal legal action and a court review of your changing financial circumstances.

Healthcare and Benefits for Older Spouses After Divorce

Older spouses are particularly vulnerable to the loss of healthcare coverage and the disruption of retirement income. These are not secondary administrative details; they are central financial planning issues that directly affect the fairness of your settlement.

Health Insurance After Divorce

You cannot remain on your former spouse’s employer-sponsored health plan once the divorce is finalized. Coverage gaps create immediate pressure, and the cost of new premiums will significantly impact your post-divorce budget. These healthcare costs must be accounted for during negotiations.

Your options for securing health insurance after divorce typically include:

- COBRA Continuation: Electing to remain on the employer-sponsored plan for up to 36 months, though you will be responsible for the full, often expensive, premium.

- Private Marketplace Plans: Purchasing individual health coverage through federal or state insurance exchanges.

- Employer-Sponsored Coverage: Obtaining a new policy through your own employer if you are currently in or returning to the workforce.

- Medicare Transition: Utilizing Medicare benefits once you reach the eligibility age of 65.

Social Security Benefits

While the Ohio divorce court does not divide Social Security benefits, you may still qualify for derivative benefits based on your former partner’s earning record. To claim these benefits, you generally must meet the following criteria:

- Length of Marriage: The marriage lasted for at least 10 consecutive years.

- Marital Status: The applicant is currently unmarried.

- Age Requirement: The applicant is at least 62 years old.

Post-Divorce Estate Planning and Beneficiary Updates

A divorce decree legally dissolves your marriage, but it does not automatically rewrite your estate plan. Post-divorce estate updates are not optional cleanup tasks; they are essential protective steps.

Failing to update these documents can leave decision-making authority and valuable assets in the hands of a former spouse. Following your divorce, you must promptly update your estate planning documents:

- Wills and Trusts: Revising your core documents to ensure your assets are distributed exactly as you intend.

- Financial and Healthcare Powers of Attorney: Revoking your former spouse’s authority to make medical or financial decisions on your behalf.

- Beneficiary Designations: Removing your ex-spouse from your life insurance policies and retirement accounts.

- Payable-on-Death Accounts: Updating the transfer-on-death instructions for your local bank accounts and investment portfolios.

Why Choose The Meade Law Group

Managing a grey divorce requires a strategic, financially sophisticated approach. At The Meade Law Group, our approach centers on protecting your long-term stability and accumulated wealth. We understand how local courts in Delaware handle complex financial divorce matters and high-asset marital estates.

We prioritize risk mitigation and asset protection to prevent avoidable financial mistakes during your settlement. Our legal counsel is designed to secure your financial independence well into retirement.

Our Services Include:

- High-Asset Property Division: Careful analysis of long-held real estate, retirement accounts, investment portfolios, and other accumulated marital assets.

- Retirement Asset Protection: Strategic handling of pensions, 401(k)s, IRAs, and QDRO-related issues to reduce avoidable losses and tax penalties.

- Spousal Support Strategy: Structuring or challenging support obligations with your long-term retirement realities in mind.

- Business and Professional Practice Valuation: Defending closely held businesses and professional partnerships against inaccurate appraisals.

- Post-Decree Modifications: Addressing support adjustments when official retirement or significant health changes occur.

Contact The Meade Law Group to schedule a confidential consultation.

Frequently Asked Questions (FAQs)

| Question | Answer |

| Is equitable distribution always a 50/50 split in Delaware County? | No. Ohio law requires that marital property be divided fairly, which does not always mean an exact 50/50 split. The court will consider the specific financial circumstances of your marriage to determine a fair division. |

| How long does a divorce take in Delaware County? | The timeline varies based on the complexity of your assets and the local court docket. Uncontested cases resolve faster, while high-asset divorces requiring business valuations, retirement asset analysis, or disputes over separate property can take significantly longer. |

| Will my spouse receive part of my retirement accounts? | Yes, it is highly likely. The portion of a retirement account or pension earned during the marriage is generally considered marital property subject to division. However, separate or pre-marital contributions may be protected if properly traced, making accurate valuation and documentation essential. |

| Can I keep the marital home after the divorce? | Yes, you can keep the home if you have the financial means to buy out your spouse’s share of the equity. However, you must carefully evaluate buyout feasibility, current refinancing realities, and ongoing maintenance costs to ensure retaining the property does not create severe liquidity strain. |

| Does retirement automatically end spousal support? | No. Retiring does not automatically stop your obligation to pay support. You must file a motion with the court to formally request a modification or termination of the order. |

| Do I need a lawyer for a divorce involving substantial assets? | Yes. The complexities of valuing businesses, drafting a Qualified Domestic Relations Order (QDRO), and managing tax consequences make professional legal guidance necessary to protect your wealth. |